Loading...

|

Content

The institutes of subsidiaries and a branch (representative office) often raise taxation issues. The reason for this is that every once in a while subsidiaries are a fiction which permits a legal form to supersede substance. I mean that it makes no overall sense to create a separate entity to split assets and liabilities of businesses that are vertically controlled. Hence, the division of businesses that belong to one UBO into legally separated entities is often formal and a fiction. After all, a legal entity is not real person but a fiction introduced and supported by law.

That is why you may often encounter discontent based on common sense rather than on law. People reprimand a multinational for all sorts of intercompany payments. They compare a family relationship with what is going on in a multinational corporation to demonstrate a lack of common

sense, e.g. to charge a royalty for the use of a tradename belonging to the parent company makes as much sense as for a case where a father charges his son a royalty for the use of his surname. There were two options to choose for regulation at the outset:

to disregard the legal form and treat a group of companies as a single person with several arms (entities), or

to disregard substance and instead to honor the legal (formal) division but to ascribe to it “arm's length”, i.e. to extend the fiction to the level where the “arms” are deemed not only legally but really independent.

The second option is the dominant one chosen in the taxation model worldwide. However, it is always challenged by arguments grounded in common sense and substance.

In taxation, a permanent establishment (PE) is the globally recognized nexus to tie a foreign entity's business to a state where part of that business is present. Another option for obtaining a relevant nexus for tax purposes is to register a subsidiary in a foreign jurisdiction. However, it could happen that such subsidiary performs functions which fit a PE rather than a subsidiary. That is where a local tax authority may come after profits of a foreign parent that are either not reflected in the tax return in the source state at all, or are included in the wrong tax return (through not being properly registered, reported, allocated and/or taxed).

That is what we are going to delve into below. We will use the soil of UAE Corporate Tax for this research.

The research has laid bare 4 major discrepancies with the OECD Model Tax Convention that haven't been addressed in the comments I have found earlier:

Two discrepancies in the Independent Agency Test;

A lack of a Control Devaluation Clause;

The absence of the Approved OECD Approach to attribute profits to a PE.

The lack of regulation does not exactly mean that an approach inconsistent with the OECD Model will be applied. Rather it entails uncertainty. In contrast, a mismatch in the Independent Agency Test triggers different effects in cases that are covered by a Double Tax Treaty (implementing the OECD model), and in cases that aren't.

Art 14(6) of the UAE Corporate Tax Law (CTL) sets forth that independent agency relief is not applicable if "... the Person acts exclusively or almost exclusively on behalf of the Non-Resident Person, or where that Person cannot be considered legally or economically independent from the Non-Resident Person”.

Let's juxtapose this with Art 5(6) of the OECD Model. Independent Agency

Relief is not allowed “where... a person acts exclusively or almost

exclusively on behalf of Non-Resident Person one or more

enterprises to which it is closely related or where that Person cannot be

considered legally or economically independent from the Non-Resident

Person[1]” (I've struck through the text which is absent

from Art. 5(6) of the OECD Model but exists in Art. 14(6) of the UAE CTL).

The difference, demonstrated above, is not always properly assessed. Some specialists opine that the CTL has just replaced “closely related person ” with “person which cannot be considered legally or economically independent from the Non-Resident Person”. However, it is not in concert with the rules cited above. Art 5(6) of the Model Convention is addressed to “closely connected persons” that are not residents of the country where the resident agent operates. The Convention's rule erases legal (formal) boundaries between closely connected non-residents in terms of assessing exclusivity. They are all to be treated as one customer to test an agent's independence.

Example 1.

Company A is a UAE resident, which is not closely connected

to any of its customers. It has plenty of customers located abroad in different

countries but all they are members of one group and meet the definition of

closely related personsAccording to Art.12(1) of the Multilateral Convention to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting (BEPS MLI) “a person is closely related to an enterprise if, based on all the relevant facts and circumstances, one has control of the other or both are under the control of the same persons or enterprises. In any case, a person shall be considered to be closely related to an enterprise if one possesses directly or indirectly more than 50 per cent of the beneficial interest in the other (or, in the case of a company, more than 50 per cent of the aggregate vote and value of the company's shares or of the beneficial equity interest in the company) or if another person possesses directly or indirectly more than 50 per cent of the beneficial interest (or, in the case of a company, more than 50 per cent of the aggregate vote and value of the company's shares or of the beneficial equity interest in the company) in the person and the enterprise”.

.

Art. 5 (6) of the OECD's Model allows all these clients to be treated as one and the agent's relationship with any and all of them to be deemed exclusive. This, in turn, allows the agent to be considered a PE of any and each of these clients.

The UAE in Art. 14 (6) of its Corporate Tax Law does not provide for such treatment. Hence, Company A may still be treated as an independent agent unless artificial segregation or other features of tax avoidance are established.

Therefore, the UAE assumes a more favorable approach here. It allows the foreign company to claim independence where an agent works on behalf of a different company of the group.

Let me factor in the recent Explanatory Guide on the Corporate Tax Law, which the MoF issued on 12 May 2023. The Comments to Art. 14 state that “the definition of Permanent Establishment in the Corporate Tax Law follows the principles provided in Article 5 of the OECD Model Tax Convention... A Non-Resident Person may consider these principles and the relevant provisions of any bilateral tax agreement... in their assessment of whether they have a Permanent Establishment in the UAE”.

This explanation does not erase the mismatches with the OECD Model addressed in this survey. The Ministry ties in the principles of the OECD with the relevant provisions of a DTT. The absence of a DTT, or a discrepancy between a particular DTT and the OECD Model, makes irrelevant the principles which are facilitated by the text of the OECD Model.

Examples given in the OECD Additional Guidance on the Attribution of Profits to

PE, BEPS Action 7 (2018) support

this position. In all three examples for a dependent agent PE the Committee on

Fiscal Affairs specifies that “there is a tax treaty in effect

. that prevents .. from taxing the business profits.., except for profits

attributable to a PE of that enterprise... Under the treaty, the profits attributable to a PE are the profits that the PE would have

derived if it were a separate and independent enterprise engaged in the same or

similar activities under the same or similar conditions, taking into account

the functions performed, assets used and risks assumed by the enterprise

through the permanent establishment and through other parts of the enterprise.

The treaty's definition of PE includes the changes to Article 5(5)

and Article 5(6)

of the MTC recommended in the

Report on Action 7"Paragraphs 60, 48 and 71.

. Therefore, it is fair to conclude that the

reference to the OECD Model and comments are relevant only where a DTT with

same wording is applicable or where pertinent provisions from the OECD Model

are included in national legislation. This survey aims to consider those

provisions of the OECD Model Tax Convention that either are absent or differ in

the UAE Corporate Tax Law. Thus, we need to analyze options which tax

administration has not bound with OECD's Model rules and comments thereto.

The Mismatch No. 1, addressed above, is a minor difference in the regulations. What else has been struck through in the UAE's Corporate Tax Law?

Let me repeat the comparison of Art 14(6) of the CTL with Art 5(6) of the OECD Model. Independent

Agency Relief is not allowed “where... a person acts exclusively or almost

exclusively on behalf of Non-Resident Person one or more

enterprises to which it is closely related or where that Person cannot be

considered legally or economically independent from the Non-Resident Person'”. I

remind that the text struck through is absent in the OECD Model but exists in

the CTL.

So, you may forget independent agency excuse if the agent “cannot be considered legally or economically independent from the Non-Resident Person”. This means that, even if a subsidiary of a non-resident in the UAE (agent) has plenty of independent principals, such agent may still not enjoy independent agency relief:

- Yes, such agent doesn't act “exclusively or almost exclusively on behalf of the Non-Resident Person ”. This part of the independence test is passed.

- But this agent “cannot be considered legally or economically independent from the NonResident Person ”. Thus, the second part of the test is failed.

Therefore, it is:

and

Example 2

Company A is a 100% subsidiary of a German company. It acts on behalf of its customers concluding certain types of contracts with customers in the UAE. 90% of its customers are independent non-residents, which is enough to qualify for independence under OECD Model.

But Germany doesn't have a Double Tax Treaty with the UAE. Thus, the UAE Corporate Tax Law is in full force here. Since, Company A “cannot be considered legally or economically independent from” the Germany parent company, the latter has a PE in the form of a dependent agent (Company A).

Art 5 (7) of the OECD' s Model sets forth: “The fact that a company which is a resident of a Contracting State controls or is controlled by a company which is a resident of the other Contracting State, or which carries on business in that other State (whether through a permanent establishment or otherwise), shall not of itself constitute either company a permanent establishment of the other”. Para 115 of the Comments to this rule explains the rationale behind it: “This follows from the principle that, for the purpose of taxation, such a subsidiary company constitutes an independent legal entity”. It also extends the term “control” used in the cited rule to cover management functions: “Even the fact that the trade or business carried on by the subsidiary company is managed by the parent company does not constitute the subsidiary company a permanent establishment of the parent company”.

The absence of the rule from Art 5 (7) of the OECD's Model in the UAE Corporate Tax Law not only exacerbates the independent agent issue considered above. It also gives rise to other issues, which may arise from running subsidiaries in the UAE. When negotiating contracts for the resale of goods purchased from a parent company or another member of the same group, a subsidiary in the UAE may face its separate entity status being challenged by the FTA for a tax purpose.

Indeed, why doesn't the UAE include in its national law provision which states that legal and economic control over the subsidiary is not enough for this subsidiary to be qualified as a PE? Is it logical to surmise that the reason is to give the FTA opportunity to treat such fact as sufficient for the qualification?

To answer these questions we need to insert the discrepancies listed above into the algorithm for recognizing a PE.

Article 5(7) of the OECD Model, skipped in the CTL, is designed to protect against giving the wrong treatment to a certain fact, namely “the fact that a company which is a resident of a Contracting State controls or is controlled by a company which is a resident of the other Contracting State, or which carries on business in that other State (whether through a permanent establishment or otherwise)”. This rule does not define what constitutes a PE. Rather, it says what doesn't.

Thus, we need to go through the attributes of a PE to pin down where it matters whether the protection given by Art. 5(7) of OECD Model exists or is absent.

The OECD saysParagraphs 116, 117 of the Comments to the OECD Model Convention.

that control over a subsidiary is to be accompanied with:

- Either any space or premises belonging to the subsidiary being put at the disposal of the parent to be used by the parent as a fixed place of its own business,

- Or the subsidiary acting on behalf of the parent and, in doing so, “habitually concluding contracts, or habitually playing the principal role leading to the conclusion of contracts that are routinely concluded without material modification by” the parent.

PE status arises only if there are the facts to fit at least one of these two options.

After that, OECD makes an exception for cases where a person in the State acts on behalf or a non-resident person as an agent. This exception covers only an independent agent, so that is the place where legal or economic dependency may matter.

Example 3

Facts

Let's use the scenario cited in the example from para 89 of the Comments to Article 5 of the OECD Model and transfer it to UAE soil.

The Subsidiary in the UAE has a Parent in Russia (there is no relevant DDT). Both are in the pharmaceutical business. The Subsidiary's representatives actively promote drugs produced by the Parent “by contacting doctors that subsequently prescribe these drugs”. The patients purchase the drugs from pharmacies. Pharmacies purchase them from the Parent or from the Parent's distributors.

Analysis

The “marketing activity” of the Subsidiary “does not directly result in the conclusion of contracts between the doctors and the Parent”. Thus, the Subsidiary is not exposed to the peril of being treated as a Dependent Agent of the Parent.

Therefore, the Subsidiary does not need independent agency

excuse. This, in turn, makes irrelevant the discrepancy in the definition of an

independent agent in the UAE Law and in the OECD Model. The absence of the

protection given to the subsidiariesSee below.

by Art.5(7) of

the OECD Model is also irrelevant.

We may see that paragraphs 5, 6 and 7 of Article 5 of the OECD Model are interrelated. The OECD Model unambiguously disallows affiliation from being treated as a sufficient factor to recognize a PE. However, Art. 14(6) of the Corporate Tax Law is also unequivocal: independent agency relief is not applicable “where that Person cannot be considered legally or economically independent from the Non-Resident Person”. In view of this, it would be inconsistent to disregard legal and actual dependency status in the regulation stipulated by the UAE Law (I mean it would make no sense to insert in Art. 14 of the CTL provision from the Art.5 (7) of the OECD Model).

***

On balance, an unfavorable discrepancy in Independent Agent

Relief may only affect a taxpayer in cases where a subsidiary or other legally

or economic controlled person in the UAE “has and habitually exercises an

authority to conduct a Business or Business Activity in the State on behalf of

the Non-Resident Person”

Art. 14(1)(b) of the Corporate Tax Law.,

i.e.:

- “habitually concludes contracts on behalf of the Non-Resident Person'” or

- “habitually

negotiates contracts that are concluded by the Non-Resident Person without the

need for material modification by the Non-Resident Person”

Art. 14(5) of the Corporate Tax Law..

A PE in the UAE is likely to be recognized in such case. But how this will affect tax obligations?

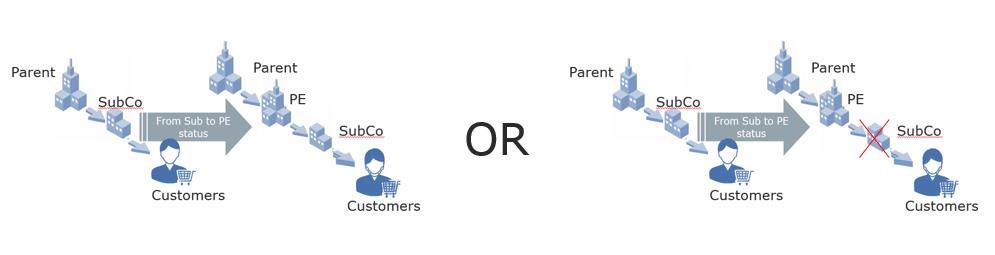

First of all, shall we:

or

In other words, shall we deem a sale to the subsidiary via a PE, or a sale to the customer via a PE?

In March 2018, the Inclusive Framework on BEPS, established by the OECD, released Additional Guidance on the Attribution of Profits to Permanent Establishments, BEPS Action 7. Paragraph 31 of this Guidance sets forth that “one of the effects of paragraph 5 [of Art.5] will typically be

that the rights and obligations resulting from the contracts to which Article 5(5) refers will be properly allocated to the permanent establishment”. Thus, the model on the right is correct and the one on the left isn't. The dependent agency model disregards the formal independence of the agent, replacing it with “deemed” PE status.

Thus, we need to:

remove from the subsidiary's tax return revenues from transactions with customers conducted on behalf of the parent and related costs, including the price paid to the parent, royalties paid, etc.,

use the excluded data to calculate the tax base for the PE with adjustments attributed to this change in status.

Art 1 2(3)(a) of the Corporate Tax Law sets out that “a Non-Resident Person is subject to Corporate Tax on ... the Taxable Income that is attributable to the Permanent Establishment of the NonResident Person in the State”.

The change of the taxpayer for these transactions “does

not necessarily mean that the entire profits resulting from the performance of

these contracts should be attributed to the PE”Para 31 of the OECD's Additional Guidance, 2018.

. Thus, tax profits gained

by contracts concluded via a dependent agent are to be allocated between the

“head- office” and the deemed PE.

Direct attribution vs “Force of Attraction”

The

Approved OECD Approach (AOA) to attribute profits to the PE disallows the

source state from taxing those profits, which are earned by the same foreign

company without the involvement of the existing PEThus, under this approach, article 7(1) does not determine the quantum of the profits that are to be attributed to the PE: all it confirms is that the right of state H is to tax only the profits attributable to the PE (and hence is a rejection of the force of attraction approach).”. P. Baker & R. Collier, The Attribution of Profits to Permanent Establishments p. 28 (IFA Cahiers vol. 91B, 2006), p. 30. It is secured by Article 7(1) of the Model Convention which sets forth: “Profits of an enterprise of a Contracting State shall be taxable only in that State unless the enterprise carries on business in the other Contracting State through a permanent establishment situated therein. If the enterprise carries on business as aforesaid, the profits that are attributable to the permanent establishment in accordance with the provisions of paragraph 2 may be taxed in that other State”.

. The

UN Model Tax Convention extends the tax base for a PE to cover profits that

haven't been earned via this PE: “The profits of an enterprise of a Contracting

State shall be taxable only in that State unless the enterprise carries on

business in the other Contracting State through a permanent establishment

situated therein. If the enterprise carries on business as aforesaid, the profits

of the enterprise may be taxed in the other State but only so much of them as

is attributable to (a) that permanent establishment; (b) sales in that other

State of goods or merchandise of the same or similar kind as those sold through

that permanent establishment; or (c) other business activities carried on in

that other State of the same or similar kind as those effected through that

permanent establishment”. This approach is widely referred to as “Force

of Attraction ” (FoA).

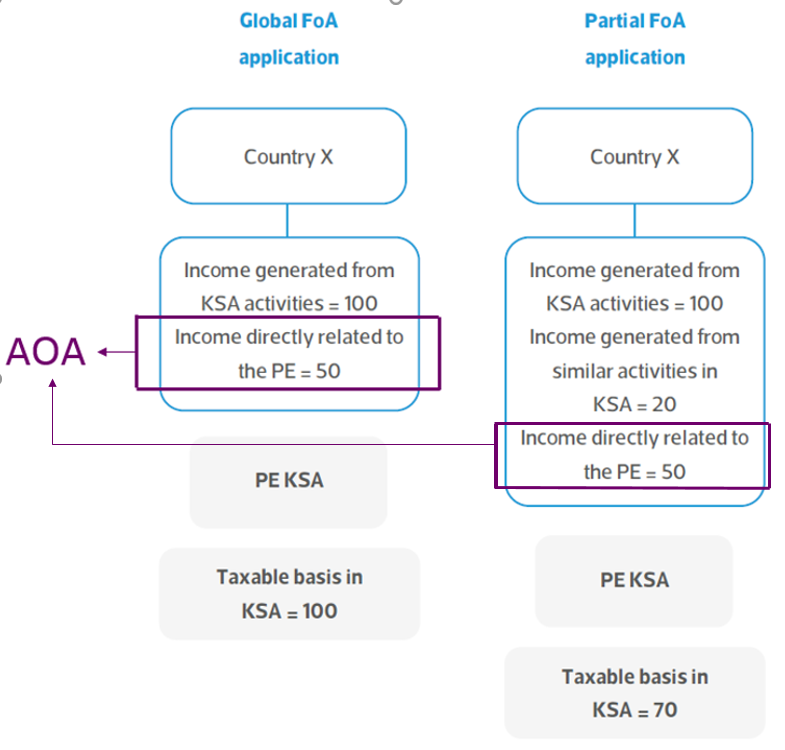

Let me exemplify the difference between direct attribution under AOA and FoA with a figure from Tax Circular No. 2104001 published in April 2021 by KSA's Zakat, Tax and Customs Authority. I have modified it with figures and text in purple to demonstrate the difference between AOA and FoA.

As you may see, AOA allows the taxation only of income directly related to the PE. It gives no authority to tax other income generated from similar activity in the source state. Conversely, FoA extends the tax base of the PE to cover income generated from similar activity in the source state without the engagement of the PE.

You may also see that the Kingdom applies the FoA approach

by default. Should it be the same in the UAE?

The answer is “No”. The UAE Corporate Tax Law does not specify directly which principle (AOA or FoA) is to be applied in the absence of a double tax treaty. However, it contains the rule that substantiates AOA in the OECD Model:

|

The UAE Corporate Tax Law, Art. 12(3)(a) |

The OECD Model Tax Convention, Art.7(1) |

|

“A Non-Resident Person is subject to Corporate Tax on the following: . The Taxable Income that is attributable to the Permanent Establishment of the Non-Resident Person in the State”. |

“If the enterprise carries on business as aforesaid, the profits that are attributable to the permanent establishment in accordance with the provisions of paragraph 2 may be taxed in that other State” |

It doesn't repeat the wording which facilitates the FoA ramification:

|

The UAE Corporate Tax Law |

The UN Model Tax Convention, Article 7(1) |

Article 5(A)(10) |

|

|

“.the profits of the enterprise may be taxed in the other State but only so much of them as is attributable to (a) that permanent establishment; (b) sales in that other State of goods or merchandise of the same or similar kind as those sold through that permanent establishment; or (c) other business activities carried on in that other State of the same or similar kind as those effected through that permanent establishment”. |

“If the income is attributable to a permanent establishment of a nonresident located in the Kingdom, including income from sales in the Kingdom of goods of the same or similar kind as those sold through such a permanent establishment, and income from rendering services or carrying out another activity in the Kingdom of the same or similar nature as an activity performed by a nonresident through a permanent establishment”. |

Therefore, the allocation of the profits to a PE in the UAE is, by default, governed by AOA, i.e. profits earned in the UAE (without a PE being involved) do not fall within the scope of Corporate Tax.See also H. Hull, United Arab Emirates: Corporate Tax Relief onInternational Investment, p. 7, 77 Bull. Intl. Taxn. 3 (2023), Journal Articles & Opinion Pieces IBFD,.

What if the UAE agreed to apply FoA in a particular double tax treaty?

Example 4

Let me use a second example from KSA's Circular mentioned above.

A company based in the UAE is providing maintenance services in KSA via its employees physically based locally for an extensive period. Based on the DTT between the UAE and KSA, the company is deemed to have a PE in KSA due to this specific activity.

The income derived from the service activity is directly attributable to the PE and therefore falls within the scope of corporate tax in KSA.

In addition to maintenance services provided with respect to specific equipment, the company is providing similar services remotely and in relation to other equipment that is located in KSA. Although this activity alone may not trigger a PE in KSA as there is no direct relation to services performed under the PE, income derived from it should still be brought within the scope of corporate tax in KSA based on the application of the FoA rule as per the DTT.

Should

we mirror this example for a PE located in the UAE? I don't think so. Article

VII (1) of the DTT between KSA and the UAE permits the parties to the DTT to tax business profit under

the FoA principle. The party may exercise this authority, as the KSA has done,

or may refrain from doing soThe legal rationale for situations like this can be found in the study performed by Rishabh Agarwal “Identifying the Mismatch: Permanent Establishment in Domestic Tax Law vs. DTAA”, [2023] 148 taxmann.com 234 (Article) . See also P. Baker & R. Collier, The Attribution of Profits to Permanent Establishments p. 28 (IFA Cahiers vol. 91B, 2006), p. 28: “As a number of the branch reports mention, a taxpayer cannot be worse off as a result of the operation of a DTC than it would be under domestic law: for those jurisdictions a DTC cannot impose a tax charge if there is none under domestic law”

Theophilou, C.A., Attribution of Profits to Permanent Establishments: Should the AOA Be Maintained as the OECD Standard? International Transfer Pricing Journal 2020 (Volume 27), No. 1...

The UAE opted for the latter. Thus, in a situation similar to the above

example, the business activity of a KSA resident in the UAE may not trigger

Corporate Taxation in the UAE “as there is no direct relation to services

performed under the PE”.

Let me give some background to explain the “new” Separate Entity Approach in the OECD Model.

In 2010, the OECD replaced Article 7 of the Model Convention with a new wording. I juxtapose, in substance, the changes in paragraphs (2) and (3) of Article 7:

" ... the profits that are attributable in each

Contracting State to the permanent establishment ... are the profits it might

be expected to make, in particular in its dealings with other parts of the

enterprise, if it were a separate and distinct independent enterprise

engaged in the same or similar activities under the same or similar conditions and

dealing wholly independently with the enterprise of which it is a

permanent establishment, taking into account the functions performed, assets used

and risks assumed by the enterprise through the permanent establishment and

through the other parts of the enterprise”;

“In determining the profits of a permanent

establishment, there shall be allowed as deductions expenses which are incurred

for the purposes of the permanent establishment, including executive

and general administrative expenses so incurred, whether in the State in which the

permanent establishment is situated or elsewhere”.

As you may see, the pre-2010 edition rather allowed the deduction of expenses actually incurred rather than an arm's length price for the consideration received from the other parts of the enterprise. The major ramifications are included in the table below11:

|

Attribution points |

Post-2010, Art 7(2) and 7(3) and OECD's comments thereto |

Pre-2010, Art 7(2) and OECD's comments thereto |

|

Royalties |

Royalties at arm's length price |

Shared cost |

|

Interest |

Arm's length interest, subject to free capital |

Shared cost, subject to free capital (but notional interest deductions are allowed for banks) |

|

Services |

Arm's length charges |

Shared cost, with markup in certain circumstances |

|

Temporary transfer of assets |

Rental fee at arm's length price |

Shared cost |

The UAE hasn't chosen any of this wording. Hence, the FTA is in position to follow any of these approaches in cases which are not covered by a DTT.

Let me dwell on it here to avoid further repetition. Some countries have implemented Art.7(2) of the OECD Model in their national legislation, e.g. Japan, Korea, Germany. Some countries haven'tSee below.. The UAE is in the second group. However, the UAE is to be distinguished from other members of this group for a lack of clarity (certainty) since no other approach is adhered to in the Corporate Tax Law. Thus, the MoF and FTA has full freedom of choice now to opt for one method of interpretation (approach) or the other.

For example, Australia, being an OECD member, doesn't apply OAO. This country has lodged a reservation against the use of the current version of Article 7 and uses the previous version of Article 7 with certain reservations. Australian tax law does not recognize dealings between different parts of one entity. Only income from, and expenditure with, other entities can be allocated to a PE. Notional transactions between the PE and the head office are not recognized as part of the attribution process. This approach is outlined in Taxation Ruling TR 2001/11.

The legal position regarding the attribution of profits to a PE is very close to that in India. India asserts that it does not follow AOA. Instead, the attribution of profits to PEs is done in accordance with Rule 10 of its Income-tax Rules, 1962, read together with the relevant DTT (if there is one).

This Rule is actually applicable to a case where tax administration “is of the opinion that the actual amount of the income accruing or arising to any non-resident person . through or from any business connection in India . cannot be definitely ascertained”. In such scenario “the amount of such income ... may be calculated” as a “reasonable'” percentage of turnover, or as “ the proportion to the total profits and gains of the business. ”, or “in such other manner as the [Assessing Officer] may deem suitable”.

The

courts in India have adopted or approved different methods of attributing

profits to PE, which range from relying on ad-hoc methods, formulary

apportionment methods, activity performed basis and, in some cases, used the

function, asset and risk approach. The courts have generally held that

attribution of profits is an exercise that would depend upon the peculiar facts

and circumstances of the case and should not be arbitrary but should be on a

fair, equitable and on a rational basis. The Courts have also held that any

finding on the question of profit attribution will involve some guesswork and

the endeavour can only be to approximate and there cannot be great precision

and exactness.See Section 8 of the Report on Profit Attribution to Permanent Establishments prepared by the Committee to Examine the issues related to Profit Attribution to PE in India and Amendment of Rule 10 of Income-tax Rules, 1962, issued for public consultation 18 April 2019.

In recent Order of the Supreme Court of India in the Civil Appeal Nos. 6511-6518/2010 of 19 April 2023 approved, in essence, arm's length approach being applied to the internal dealing of the deemed PE and other parts of the same entity:

- The remuneration for the activity of the deemed PE is to be measured Arm's length and

compared with compensation actually paid and taxed.

- If the latter is equal or higher the former, the attribution complies with Explanation 1(a) under clause (i) of Sub-Section (1) of Section 9 of the Income Tax Act. It reads as follows: “. in the case of a business other than the business having business connection in India on account of significant economic presence of which all the operations are not carried out in India, the income of the business deemed under this clause to accrue or arise in India shall be only such part of the income as is reasonably attributable to the operations carried out in India”.

India's situation is quite similar now to the current situation in the UAE as the solution in both countries may only be found by applying one way (approach) to interpret the law or another. However, in India you may find support in case law. This is not yet the case in the UAE.

Art. 7(2) of the UN Tax Model Convention sets out that “subject to the provisions of paragraph 3, where an enterprise . carries on business . through a PE situated therein, there shall . be attributed to that PE the profits which it might be expected to make if it were a distinct and separate enterprise engaged in the same or similar activities under the same or similar conditions and dealing wholly independently with the enterprise of which it is a PE”.

Paragraph 3 of this Article shows that treatment as “a distinct and separate enterprise . dealing wholly independently with the enterprise of which it is a PE” doesn't necessarily imply arm's length to measure the input of the head-office in the joint activity: “In the determination of the profits of a PE, there shall be allowed as deductions expenses which are incurred for the purposes of the business of the permanent establishment including executive and general administrative expenses so incurred, whether in the State in which the PE is situated or elsewhere. However, no such deduction shall be allowed in respect of amounts, if any, paid (otherwise than towards reimbursement of actual expenses) by the PE to the head office of the enterprise or any of its other offices, by way of royalties, fees or other similar payments in return for the use ofpatents or other rights, or by way of commission, for specific services performed or for management, or, except in the case of a banking enterprise, by way of interest on moneys lent to the PE. ”.

As we found above, the UAE does not include AOA in the Corporate Tax Law. Hence, it is subject to interpretation which model (the OECD, UN or another) to choose for attribution. The FTA is free to choose the UN approach in cases where AOA or a similar pattern is not ordained by a DTT.

The practical difference between these two approaches is crucial. A PE's profit under AOA is hypothesized as that of a separate enterprise and may earn profit where the whole legal entity incurs losses. This is incompatible with the “single enterprise” (“relevant business activity”) approach where the share of an entity's (as a whole) profit is subject to attribution.

Under AOA, a PE may earn profit on its transaction with the remaining part of the enterprise. No such profit may be recognized once the single enterprise approach is adopted.

Again, the UAE Corporate Tax Law doesn't restrict the FTA from applying any of these approaches to interpreting Art.12(3)(a) of the Law.

These two conceptions differ in the treatment of such component of Arm's Length as the allocation of risks. The principal idea of the “Single taxpayer” concept is that a PE is not able to bear a risk. The latter may be only assumed via a legally binding act (contract). Regardless of how much the PE is involved in negotiating or performing a contract, it may not assume any legal obligation. Only a legal entity has such ability.

Therefore, remuneration for risks under a PE's activity are always attributed to the head office. What is then left to be attributed to the PE? Assets and functions involved in the activity of a PE on behalf of the principal. If these are properly factored into the calculation of the price (fees) paid by the principal to dependent agent, there is nothing to add to the tax base in the source state. Indeed, if functions and assets used by the dependent agent have already been measured at arm's length in the contract with principal, the profit attributed to the PE for these functions and assets calculated on the same principle will also be the same.

The “Dual entity” concept treats the allocation of risk in an economic rather than a legal way. Here the risks stick to the functions, i.e. to the people involved in risk management. If a dependent agent has employed or outsourced people who manage at least part of the relevant risks, then at least part of the correspondent tax base has to be additionally transferred to the source state from the head office.

In

my opinion, the “single taxpayer” approach fits better with the OECD's TP GuidanceOECD, Committee on Fiscal Affairs. Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations (Paris: OECD, 2022)

. It distinguishes the assumption of risks from risk

managementAccording to Para 1.63 of the Guidance “Risk management is not the same as assuming a risk. Risk assumption means taking on the upside and downside consequences of the risk with the result that the party assuming a risk will also bear the financial and other consequences if the risk materialises. A party performing part of the risk management functions may not assume the risk that is the subject of its management activity, but may be hired to perform risk mitigation functions under the direction of the risk-assuming party. For example, the day-to-day mitigation of product recall risk may be outsourced to a party performing monitoring of quality control over a specific manufacturing process according to the specifications of the party assuming the risk”.

. The latter deserves fair compensation as a function within arm's length. The

former is a subject for remuneration for the fact of the risk being assumed.

Risk may be assumed by a responsible party. A single legal entity is

responsible, which comprises all its parts (branches, offices, etc.) but not a

dependent agent PE (a separate entity).

Thus, a dependent agent PE may deserve arm's length remuneration for a risk it has assumed only where such agent legally assumes the risk via a contractual arrangement or where this agent is responsible or co-responsible for an act (event). When this is the case, a dependent agent has the ability to assume the risk (as a full-fledged legal entity). If it exercises this authority, its remuneration should factor risk in to comply with the arm's length principle. A Transfer Pricing adjustment may be applied in a case of non-compliance. Therefore, requalification as a PE doesn't create an additional tax base for the state.

Example 5

Let's take the 4th example from the Additional Guidance.

Facts.

TradeCo, a company resident in Country R, has as its core business the procurement and sale of widgets. BuyCo, a commonly owned company resident in Country S, performs procurement activities on behalf of TradeCo in Country S, purchasing widgets as agent on behalf of TradeCo, and in the name of TradeCo, from unrelated suppliers in Country S. BuyCo does not own the widgets at any point, nor does it have any entitlement to the amounts paid by TradeCo's customers for the widgets procured by BuyCo. Those amounts belong to TradeCo.

Personnel of BuyCo are responsible for warehousing the inventory and determining and monitoring the appropriate inventory levels.

TradeCo pays BuyCo a commission equal to a percentage of the cost of purchases made by BuyCo on behalf of TradeCo in Country S. BuyCo's business consists solely of its activities for TradeCo. TradeCo has no operations of its own in Country S.

Analysis in the Additional Guidance

Para 74 says that “under Article 9, the remuneration that TradeCo pays to BuyCo is found to be at arm's length taking into account its functions performed, assets used and risks assumed”.

In para 77, with reference to the AOA, the

actual dealing (commission) between TradeCo and BuyCo has been requalified

(‘hypothesized') as “the sale of inventory by the PE to the head office”See my opinion on this type of the requalification below.

.

Then, “under step two of the AOA”, the TP guidance “is applied by analogy to determine the arm's length pricing of

the internal dealing between the PE and the head office. In this case, such pricing

would equal the amount that TradeCo would have had to pay if it had purchased

the widgets from an unrelated supplier performing the same functions in Country

S that BuyCo performs on behalf of TradeCo (attributing to such supplier

ownership of the assets of TradeCo related to such functions, and the

assumption of the risks related to such functions”.

According to para 79 of the Additional Guidance, “in its tax computation, the PE will deduct the amounts paid for the widgets in Country S and other expenses incurred by BuyCo in performing the procurementfunctions for TradeCo, as well as the remuneration paid to BuyCo, as well as other expenses wherever incurred for the purpose of the PE”. Analysis of the Analysis

What in this example may not be addressed by the

tax administration in Country S without requalification as a deemed PE? An

accurately delineated actual transaction is to be assessed as an arm's length

transaction. If the functions and allocation of risks fit the purchase and

resale activity, this actual (underlying) structure has to be addressed in the

tax computation Paragraphs 1.36 and 1.98 of the OECD TP Guidelines.

.

The dependent agency PE tool is not necessary for this.

Therefore, in my opinion, the same outcome may be gained in Country S within the TP rules on their own. There is no need to refer to regulation on a dependent agency PE.

Anyway, the FTA may assume any of these approaches to surcharge. In most cases, dual entity approach would allow to transfer more tax base in the UAE. Thus, application of this approach in course of the audits is more likely.

Example 2 considered in paragraphs 47-58 of the Additional Guidance shows

that AOA may lead to a requalification of the transactionExample 3 considers a similar requalification for a case where compensation has been paid to the dependent agent as service fees (paragraphs 59-69 of the Additional Guidance).

. In this example the commissioner

(SellCo) acting in his own name but on behalf of a foreign principal (TradeCo)

distributed products belonging to the latter and supplied to customers directly

by the Principal.

In the fiction of a deemed PE this relationship has been requalified (“hypothesised”) in “the sale of the goods by the head office to the PE” to attribute the profits. The rationale for this is given in para 53 of the Additional Guidance: “The functional and factual analysis also demonstrates that the significant people functions relevant to the assumption of inventory risk and to the disposition of the inventory are performed by the personnel of SellCo on behalf of TradeCo in Country S. Accordingly, the PE is hypothesised to be the economic owner of the inventory and the party assuming the inventory risk”.

This example is not perfect, in my opinion. I think that if facts fit the sale model, you should repeat the dependent agency test. The re-seller acts on its own behalf, which overturns formal compliance with the definition of a “dependent agent”. Hardly should the dependency test be built on the form taking priority over the substance. In the OECD's example, the source state does not need the dependent agency tool to surcharge SellCo. It may simply apply arm's length to the functions actually performed by SellCo, the actual allocation of risk management functions and the assets used.

The reverse situation, where the sale model is requalified as agency, may be a better example. However, even the reverse example should not give rise to an increase of the aggregated (PE + entity) tax base, if the dependent agent was compensated at arm's length for his activity on behalf of the foreign “principal”.

Indeed, the application of Article 7(2) of the OECD

Model to the dependent agent means

that “the profits to be attributed to the permanent establishment . are only

those that the permanent establishment would have derived if it were a

separate and independent enterprise performing the activities that the

dependent agent performs on behalf of the non-resident enterprise”.Para 31 of the Additional Guidance.

Thus, requalification as a PE under the OECD model should only make sense where the subsidiary hasn't yet recognized income earned on the operations performed on behalf of the Company. If subsidiary is already included in the chain of transactions and has received arm's length remuneration for its functions in this chain, the taxable base of the PE will be the same as the tax base of the subsidiary.

Example 6

Facts

A foreign company (the Parent) is tax resident of Kazakhstan. It has a 100% subsidiary (SubCo) in the UAE acting as a local distributor for goods, which SubCo purchases from the Parent and resells to independent customers in the UAE.

Under these contracts, the Parent delivers these goods directly to the independent customers.

The purchase price for the goods has actually been determined as the resale price minus an agreed fee. The latter has been determined Cost+, i.e. expenses incurred + mark-up.

SubCo neither assumed the real inventory risk, nor managed it. All risks corresponding to the sale contracts with customers have actually been managed by the Parent company's employees.

Analysis

According to Art. (5)(a) of the DTT between the UAE and Kazakhstan, a resident's activity is to be deemed a PE if “he has and habitually exercises in the first-mentioned Contracting State a general authority to negotiate and conclude contracts for, or on behalf of, such enterprise”.

Parent and SubCo entered into a purchase and sale agreement (PSA). However, their actual relationship and subsequent performance of the contract fits the agency model, i.e. the Parent actually instructed SubCo to find potential customers and negotiate contracts with them in the name of SubCo but (actually) on behalf of the Parent for the Parent to subsequently perform such contracts directly to the customer.

SubCo included in the Corporate Tax Return the whole amount of revenues received from the customers and deducted the purchase price paid to the Parent.

In this example, the transfer of the operations from SubCo's tax return to the tax return of the PE doesn't change the amount of the tax base. In tax return, agency fees must be included which are an exact match for the difference between the resale and purchase price earlier included in SubCo's tax return. There could be a potential mismatch only if the purchase price doesn't meet the arm's length standard.

The same outcome may be illustrated by Example No. 3 of the Additional Guidance.

Example 7Based on Example No. 3 in the Guidance (paragraphs 59-69)

An associated Resident performed marketing activities on behalf of a Non-Resident under a services agreement. The Resident's fee was equal to a percentage of the sales revenue received by the Non-Resident from sales of advertising space to customers, which the Resident negotiated to enter into a contract with the Non-Resident.

According to the actual functions of the parties, the marketing service contract has been requalified (“hypothesized”) as a sale of advertising space by the head office to the PE. The sales to customers are transferred into a sale of the PE.

However, the remuneration in terms of the service fee actually received by the Resident is equal to the difference between the hypothesized purchase, measured at arm's length, and the resale price. It may only differ if contractual service fees are not in line with the arm's length principle. But, in such a case, a surcharge would be triggered by TP regulation rather than requalification as a PE.

Example 8

The facts are the same as in Example 6 or 7, except for one: the Resident and its Parent haven't concluded any agreement to remunerate the Resident. The contracts with customers have been concluded directly between the Parent Company and an independent customer.

Here the requalification as a PE generates an additional tax base since the Resident hasn't included in its tax return profit attributed to its contribution to the sales.

The examples above demonstrate that the requalification of a subsidiary as a PE does not affect the tax base since the tax base has to be calculated for a PE in line with AOA. The OECD noted this effect in para 42 of the Additional Guidance: “It should be noted that the host country's taxing rights are not necessarily exhausted by ensuring an arm's length compensation to the intermediary. As noted earlier, one of the elements to determine and deduct in calculating the profits attributable to the PE is an arm's length reward to the intermediary. Depending on the facts and circumstances of a given case, the net amount ofprofits attributable to the PE may be either positive, nil or negative (i.e., a loss). In particular, when the accurate delineation of the transaction under the guidance of Chapter I of the TPG indicates that the intermediary is assuming the risks of the transactions of the non-resident enterprise, the profits attributable to the PE could be minimal or even zero”.

However, these examples cover the cases where a Double Tax Treaty (DTT) has a provision similar to the rule provided for in Art. 7(2) of the OECD's Model. What if in Example 5 we replace the tax residency of the Parent with Germany or another country that does not have a DTT with the UAE?

Germany's national regulation treats a permanent establishment like a separate and independent entity for tax purposes. In other words, Germany has implemented AOA in its legislation. Thus, the absence of a DTT between Germany and the Emirates does not matter for UAE residents that have a deemed PE in Germany.

However, AOA is not included in the UAE Corporate Tax Law. Article 24(4) of this law “approves” a similar approach to calculating exempted profit of a foreign PE of a UAE Resident: “In determining the income and associated expenditure of a Foreign Permanent Establishment, a Resident Person and each of its Foreign Permanent Establishments shall be treated as separate and independent Persons”. Therefore, this regulation does not affect the attribution of the profit of a Non-Resident's PE in the UAE.

The MoF has just issued its Explanatory Guide on The Corporate Tax Law. The guidance to Article 14 sets forth that “the criteria set out in this Article also apply when determining the existence of a Foreign Permanent Establishment for the purposes of Article 24”. It does not help much to substantiate the application of AOA from Art. 24 to a PE located in the UAE since we need to justify interchangeability within Art. 24, where AOA is ordained for a foreign PE, and Art. 12(3)(a), where AOA is missing for a local PE.

Thus, there is no certainty now as to whether or not the FTA will follow the OECD's approach for attributing profits to a deemed PE. It is bound to do so not in legal terms, but through good will and common sense only. If the FTA applies a different approach, the tax base may change for a deemed PE even in a case where subsidiary receives arm's length compensation.

Example 9

The facts are the same as in Example 6 except for the tax residency of the Parent, which is now Germany. And let's add a royalty to the picture, which SubCo paid to the parent for the use of trademarks in transactions actually made on behalf of the Parent and using the Parent's trade name in the name of the Subsidiary.

The FTA may try to disregard the royalty. The rationale could be that the royalty does not make sense in the relationship between the entity and its PE. The FTA may also refer to the UN Tax Model to back up this idea.

The OECD's approved approachParas 203, 204 and 206 of the 2010 Report on the Attribution of Profits to Permanent Establishments.

rebuts such an

interpretation. However, it is binding only in situations covered by the

relevant DTT. The Germany-UAE case is not covered.

In a potential tax dispute, a taxpayer may find support in Art. 35(1)(d) of the CTL which prescribes treating “a Person and its Permanent Establishment or Foreign Permanent Establishment” as “Related Parties”. You may then move over to Art. 34(1), which states that “in determining Taxable Income, transactions and arrangements between Related Parties must meet the arm's length standard...”. Thus, the transaction and arrangement between foreign entity is recognized, as is their use of the arm's length standard.

However, Art. 34(2)of the Law envisages that “a transaction or arrangement between Related Parties meets the arm's length standard if the results of the transaction or arrangement are consistent with the results that would have been realised if Persons who were not Related Parties had engaged in a similar transaction or arrangement under similar circumstances”. Again, the FTA may take the position that “Persons who were not Related Parties” had never “engaged in a similar transaction”, i.e. a transaction where the head-office charges a royalty to its branch/office for IP that belongs to the whole company (entity). The tax authority may reinforce this argument referring to the UN Tax Model.

In my opinion, this argument (of the tax authority's) doesn't make sense since this way of thinking compromises the purpose of Art. 35(1)(d) and Art. 34(2): what transactions and arrangements might pass the arm's length test, then? One part of the company would hardly pay another part of the same company because, legally and in actual fact, only one person exists. Therefore, it seems obvious that fiction is meant, namely the fiction which obliges the PE and head office to be treated as separate but related persons.

The Corporate Tax Law provides for some advantages for UAE residents only. In such cases, the requalification of a resident as a deemed PE may deprive the resident subsidiary of such advantages.

The impact on Small Business, a Tax Group and Tax Loss Transfer Reliefs

In particular, this concerns:

Small Business Relief (Art. 21(1) UAE CTL),

Intra-Tax Group Operations Relief (Art. 40(1)(a) UAE CTL),

Tax Loss Transfer Relief (Art. 38(1)(b) UAE CTL).

The status of a dependent agent does not negate the identity of the resident as a legal person registered in the state. Therefore, the dependent agent has dual status:

- it is a legal person and resident of the UAE, and

- it is a Permanent Establishment of another (foreign) person.

Therefore, the activity of the resident will be allocated between these two identities, i.e. tax-relevant incomes and expenses will be allocated between the PE (non-resident) and legal person (resident). Thus, the latter is not disqualified from the above-mentioned reliefs allowed to residents. Rather, this relief doesn't cover part of the income attributable to the non-resident.

Example 10

A Resident acts as dependent agent on behalf of a Group Company. The revenue attributed to this activity is AED 2 mln. The remaining 1 mln relates to the activity of the Resident which doesn't fall within the definition of a dependent agent.

The Resident applied Small Business Relief and paid zero tax on the whole profit earned.

The FTA is entitled to remove 2 mln from the scope of this relief and attribute it to the dependent agent PE. Since a Non-Resident person may not apply Small Business Relief, this sum of 2 mln may be taxed at 9% after deduction of the pertinent costs.

Example 11

Let's use the previous example but increase the numbers:

- the total revenues are 5 mln,

- the revenues from activity which pass the dependent agency test are 2 mln,

- the revenues from activity which doesn't fall within the scope of the deemed PE are 3 mln.

The Resident may save from voluntarily attributing profits to the tax return of the dependent agent PE. Profit pertinent to 3 mln falls under Small Business Relief. This Relief may not be applied without separation for total revenue exceeding the 5 mln threshold set by the Minister.

On balance, only 2 mln (minus deductible costs) transferred to the PE tax return stays taxed.

Example 12

Facts

The FTA established that a Company is a member of the Tax Group. An audit laid bare certain activity performed by this Company on behalf of a foreign person, which

meets the definition of a dependent agency PE. There ensued an allocation to the PE of a certain amount of the Company's revenues and pertinent costs.

Analysis

Art. 40(1)(a) of the UAE CTL hinders non-residents from joining a tax group. Taking into account the dual status of the dependent agent entity, this entity (as a resident) may join a tax group. However, revenues and costs related to PE activity may not be included in a consolidated tax return of the tax group.

Example 13

Facts

Part of the activity of the Resident Company involves acting on behalf of the foreign parent and part doesn't. In year 1 this Resident earned profit for the dependent agency PE but a loss for the rest of its business. In year 2 the results were the opposite: a loss for PE activity and profit from the rest.

Analysis

Art. 38(1)(b) of the Corporate Tax Law allows losses to be transferred between residents only. Therefore:

the Resident may not balance profit it earned as a PE with losses incurred by the rest of its business. The Resident may deduct these losses against its profit in the 2nd year, calculated separately from the PE;

the losses incurred from the PE's activity in the 2nd year may not be deducted from the profit earned in the same year from other business of the Resident. These losses may be only be carried forward to be deducted from the PE's profits in subsequent periods.

Article 22 (1) of the Corporate Tax Law exempts “dividends and other profit distributions received from a juridical person that is a Resident Person”. Requalification of “a juridical person that is a Resident Person” as a permanent establishment of the Non-Resident Person exposes the dividends received by the resident co-shareholder.

Example 14

Company S is a UAE resident. 96% of its shares belongs to a Non-Resident (Company N) and 4% to the UAE Resident (Company R). Dividends to be paid to the resident co-shareholder shall be exempted from Corporate Tax only if Company S is a resident. If the dividends have been paid from the profit of the Company S, requalified as the profit of its foreign shareholder (Company N), the UAE resident (Company R) is at risk of having 9% tax assessed, because the dividends:

do not qualify for exemption given by Art. 22 (1) of the UAE CTL, and

do not meet the conditions to apply the participation exemption (Art. 23(2)(c) requires investment in at least 5% of the shares of the foreign company).

The OECD clarifies that “a number of countries actually

collect tax only from the intermediary even though the amount of tax is

calculated by reference to activities of both the intermediary and the Article 5(5) PE”Para 44 of the 2018 Additional Guidance.

.

The meaning is that it may be beneficial to allow the deemed PE's profit and

profit from other activity of the resident (the dependent agent) to be reported

in one tax return.

In

its 2018 Additional

Guidance, the OECD in all three examples, illustrating the attribution of

profits to a deemed PE, reiterates that “for reasons of administrative

convenience, the tax administration . may choose to collect tax only from SellCo even

though the amount of tax is separately calculated by reference to the tax

liability of SellCo and the PE”Para 57 of the 2018 Additional Guidance. The same remark is given in paragraphs 69 and 80.

.

However,

this would hardly be chosen as a solution owing to the issues considered above.

In its 2010 OECD 2010 Report on Attribution of

Profits, the OECD emphasizes that such

simplification is pertinent to simplify the administrative burden. The

simplification “should also ensure that any other tax consequences arising

from different rules for PEs and subsidiaries in the PE jurisdiction are taken

into account”.Para 246 of the 2010 Report.

On the other hand, the OECD:

- Stresses that formal recognition of two different legal entities (the dependent agent PE and the dependent agent enterprise) minimizes “the danger of overlooking the assets used and risks assumed in the performance of the functions in the PE jurisdiction”;

- Says that the requirement to file standalone tax returns for a deemed PE is one way to secure such formal recognition.

Thus, I think that even if the FTA allows one tax return to be filed for a dependent agent PE and one for the pertinent entity, this may only affect the procedure. The tax base and benefits under the Corporate Tax Law would be most probably be addressed in the same way as if such PE's profit is reported separately.

The deduction of the tax base declared by the resident (dependent agent) from the income attributable to the deemed PE could serve as a remedy that is more feasible. The OECD mentions such deduction several times in the Additional Guidance: “The arm's length reward to the intermediary for the services it provides to the non-resident enterprise is one of the elements that needs to be determined and deducted in calculating the profits attributable to the PE under Article 7”.Para 33. See also para 42 cited above in the Section ‘Requalification in course of Attribution'. The deduction is also mentioned in the examples which OECD gives for a dependent agent PE (paragraphs 56 and 61).

However, a lack of the attribution rules, similar to the Art. 7(2) of the OECD Model, in national law may prevent recourse to the OECD's comments thereto. Non-residents from states with a DTT based on the OECD Model may be safe in relying on these comments.

Federal Decree-Law No. 28 of 2021 and Cabinet Decision No. 49 of 2021 hold tax persons accountable for:

- “Failing to submit a Tax Registration application”. The failure to apply for registration of a PE may result in a penalty of 10 000 AED.

- The failure to submit a Tax Return. A Non-Resident failed to file a tax return for its dependent agency PE and exposed itself to a penalty of 1,000 AED for the first time and 2,000 AED in case of a repeat within 24 months.

- The submission of an incorrect tax return by a Subsidiary, i.e. a return with profits which are to be attributed to different taxpayer (to the PE of a Non-Resident) - 1,000 AED for the first time and 2,000 AED in the case of a repeat, etc.

We may not exclude a formal approach to the assessment of fines calculated out of the amount of underpaid tax. The amount paid by a subsidiary which incorrectly united its tax base with the base attributable to a PE may be the same as the aggregate amount as correctly reported in standalone tax returns. However, the auditors may allege that such subsidiary overpaid corporate tax and may claim a refund. The non-resident failed to pay this amount. The result for the state's coffers is the same in terms of the balance of tax to be refunded and paid. Nevertheless, the FTA may try to collect a penalty for violation No. 12 in Table 1 annexed to Cabinet Decision No. 40 of 2017 amended by Cabinet Decision No. 49 of 2021.

Violation No. 12 is described as “the failure of the Registrant to calculate Tax on behalf of another Person where the Registrant Taxable Person is obliged to do so under the Tax Law”. There's no specific rule in the Corporate Tax Law which obliges a resident who is a dependent agent for a Non-Resident to calculate tax for the other taxpayer (the foreign company). However, the tax authority may refer:

to the fact that the activity of the subsidiary acting on behalf of the agent entailed a taxable operation of another person;

to the dual identity of the dependent agent, i.e. one and the same resident person is also deemed a PE of the foreign person and therefore is responsible for calculating tax on behalf of the company of which the PE is a subsidiary.

Simplifying the administrative procedure, as recommended by the 2010 OECD 2010 Report on Attribution of Profits, reiterated in the Additional Guidance and consideredabove, may be a perfect solution to these issues. Collecting tax calculated in one tax return but separately for a foreign PE and for the rest of the resident's operations would relieve the administrative burden only. It does not affect the total amount of tax to be paid. Hence, if the Minister, FTA or the Cabinet let a dependent agent resident report profits for both statuses in one tax return, such permission would be fully in line with the OECD guidance.

***

Warning: Pursuant to MoF press-release issued 19 May 2023 “a number of posts circulating on social media and other platforms that are issued by private parties, contain inaccurate and unreliable interpretations and analyses of Corporate Tax”.

The Ministry reminded that official sources of information on Federal Taxes in the UAE are MoF and FTA only. Therefore, analyses that are not based on official publications by MoF and FTA; or have not been commissioned by them, are unreliable and may contain misleading interpretations of the law.

See full press release here.

You should factor it in dealing with this article as well. It is not commissioned by MoF or FTA. Interpretation, conclusions, proposals, surmises, guesswork, etc. it comprises have status of the author's opinion only. Like any human job, it may contain inaccuracy and mistakes that I have tried my best to avoid. If you find any inaccuracies or errors, please let me know so that I can make corrections.